Making one payment towards your debts can sound like the perfect solution, but not all “one payment” options are the same.

In the debt review industry, people often talk about a single or consolidated monthly repayment, which can easily be confused with a consolidation loan. This confusion can lead to poor decisions if the difference is not clearly understood. Many consumers hear similar language and assume the outcomes are the same. They are not.

Here is how to tell them apart.

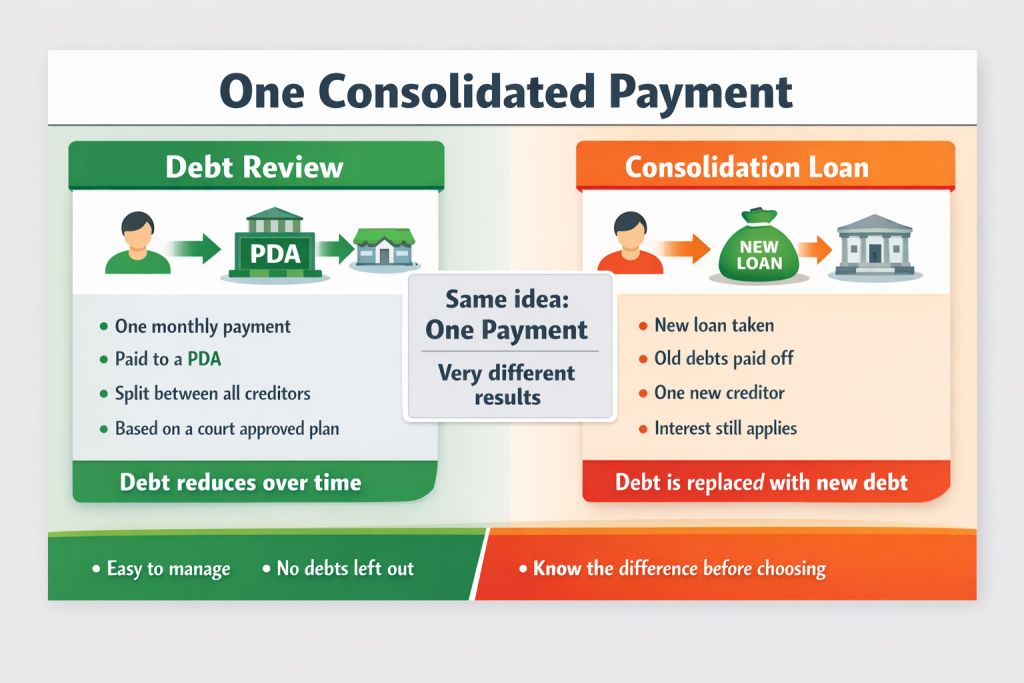

In debt review, the idea of one payment is about making your life simpler and more manageable. Instead of trying to keep up with multiple payments to different credit providers, you make one monthly payment to a Payment Distribution Agent (PDA). The PDA then takes care of the rest. They split your payment between your credit providers based on a debt restructuring plan that has been worked out on your behalf.

This restructuring plan is carefully designed. It is put together based on what you can realistically afford. It is discussed with your credit providers and, later made into an official court order. This gives the plan structure and legal backing. It also ensures that every credit provider is included and that no debt is left unpaid or ignored.

One of the most important points to understand is that debt review does not involve taking on new credit. You are not getting a new loan. You are repaying your existing debt in a more structured way. Over time, as you continue to make your payments, your debt reduces until it is fully paid off.

A consolidation loan works in a very different way. It is a new loan that you take out from a credit provider. The purpose of this loan is to pay off your existing debts with other credit providers so that you are left with only one account to manage. While this may seem convenient, it is still a form of credit. You are still borrowing money and you are still paying interest on that loan. In many cases the interest fees can be very high.

In some cases, a consolidation loan can even increase the total amount you repay, especially if the repayment period is extended. All that also depends on whether you qualify for the loan in the first place, which is based on your credit profile and affordability at the time. It might be that the new credit provider does not want to take you on as a client.

The reason people get confused is because both options talk about one monthly payment. Both seem to bring different debts together into a single arrangement. But the way they work and the results they produce are very different.

With debt review, one payment makes things easier to manage. It helps ensure that all your debts are paid in a fair and structured way. You do not have to worry about missing payments to different credit providers. The PDA handles the distribution, and everything follows a clear plan.

The real benefit is that this plan is focused on helping you become debt free over time. It is not about adding more debt. It is about dealing with what you already owe in a realistic and sustainable way.

At the end of the day, both options may sound similar, but they are not the same. A consolidation loan means taking on new debt. Debt review means working your way out of debt. Knowing the difference can help you choose the path that truly improves your financial situation.